Corredor Bioceánico and Mercosur Location Strategy

What the Brazil–Paraguay–Argentina–Chile corridor changes for companies evaluating logistics, production sites, market entry and export routes in Mercosur.

Business implication

- Model the corridor as optionality, not as secured capacity.

- Road completion and border operations remain gating factors.

- Benefits are sector-, route- and location-specific.

- Atlantic routes remain dominant for many companies.

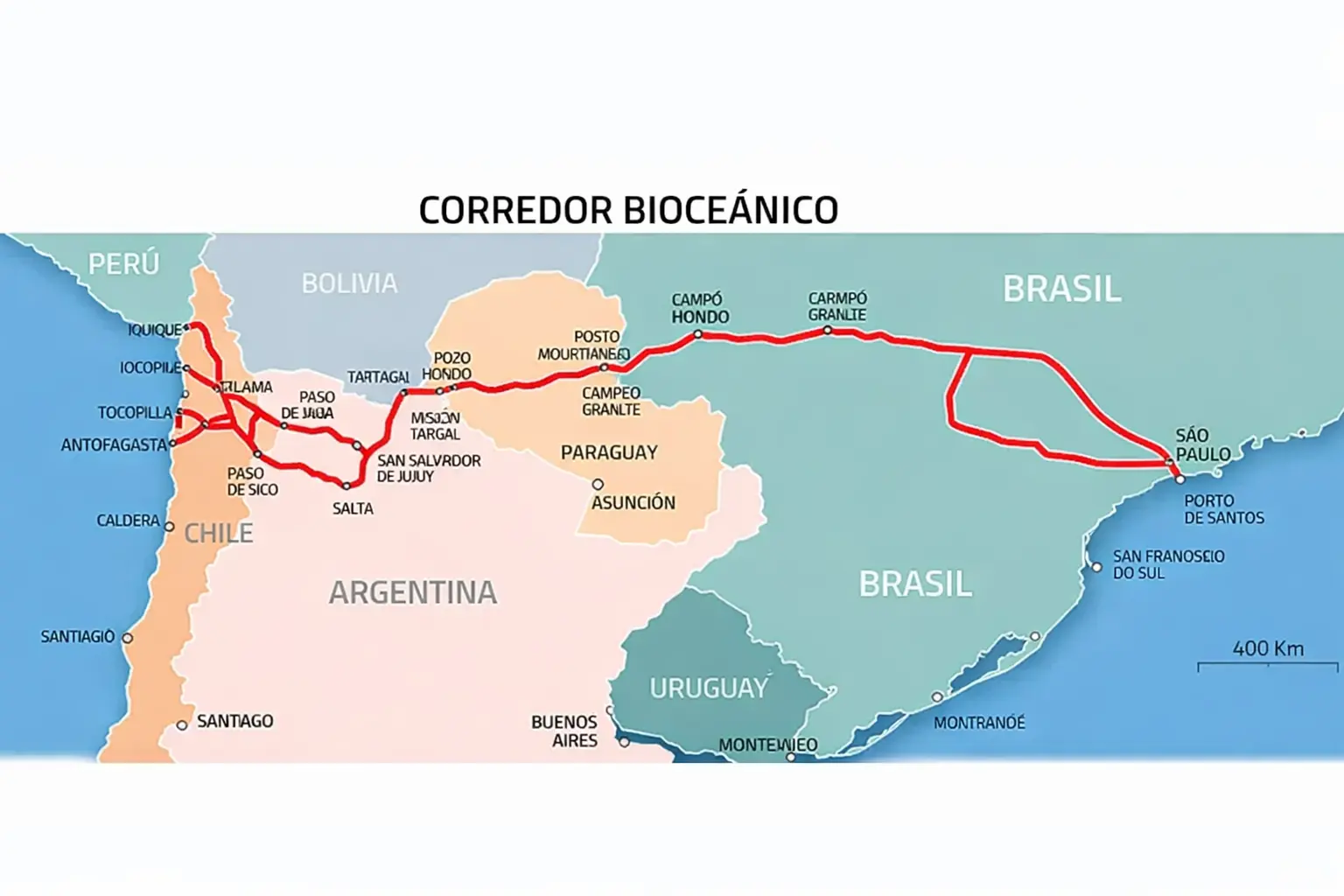

The Corredor Bioceánico Vial is a roughly 2,400 km road axis linking Mato Grosso do Sul in Brazil through Paraguay and northern Argentina to Chilean Pacific ports. Based on the project status assessed in this article, it should not drive a 2026/27 location decision on its own. Its strategic value lies in future optionality: alternative Pacific access for selected export flows, stronger relevance for corridor-adjacent regions and a possible change in location economics if missing infrastructure, customs processes and private investment materialize.

The corridor is being built, but regular volume logistics still depends on missing sections, customs procedures and private investment.

Companies should model corridor scenarios, but avoid basing location decisions on government communication alone.

Agro, mining and logistics are more exposed than general industrial production focused on Atlantic or EU routes.

Use the corridor as one variable in a wider Mercosur location review

This article provides a regional screen. A company-specific decision must also compare Atlantic and Pacific routes, customer and supplier geography, customs exposure, local incentives, workforce, site economics, sales access and the ability to operate across borders.

How the corridor changes Mercosur location decisions

Geographic Axis: Brazil–Paraguay–Chile

The Corredor Bioceánico connects four countries at different stages of completion. Brazil is largely operational, Paraguay is closing its section by the end of 2026, and Chile is infrastructure-ready with port modernisation underway. The critical bottleneck is Argentina.

Ruta Nacional 51 between San Antonio de los Cobres and Paso de Sico still lacks 134 km of full asphalt. The route is currently passable with construction machinery and limited freight, but not suitable for regular volume logistics. Salta has applied for Fonplata financing, with construction start expected in 2026 and full completion at the earliest in 2028.

Export Logic: Atlantic vs. Pacific

Currently, Mato Grosso do Sul exports via Santos and Paranaguá on the Atlantic side to Asia via Cape Town or the Panama Canal. With the Corredor Bioceánico via Antofagasta, the route would shorten considerably. Logistics costs are estimated to fall, mainly through shorter sea freight times and avoided canal fees.

Paraguay gains a strategic advantage because direct Pacific access reduces dependence on Argentine intermediary ports or Brazilian Atlantic routes. For a landlocked country, this is more than a transport improvement — it changes the range of possible export routes.

For Chile, the corridor means northern ports such as Antofagasta and Iquique can become hubs for Brazilian and Paraguayan agricultural exports. But this depends on actual freight volume, port capacity and the ability to handle sustained cross-border flows.

Affected Sectors

Soybeans, corn and beef

Main beneficiaries are processors and exporters near the corridor with Asia-bound exports from Mato Grosso do Sul and Paraguay.

Cargill, ADM, COFCO and Louis Dreyfus already control large parts of Paraguay's soybean exports and may reposition logistics hubs accordingly.

Lithium, copper and iron ore

Northern Argentina and the Paraguayan Chaco hold exploitable deposits. Infrastructure can reduce logistics friction, but commodity prices, water availability and permits remain decisive.

Road access is necessary, but not sufficient.

Forwarders, customs and hubs

Freight forwarders, customs brokers and port operators are direct beneficiaries if regular freight flows emerge.

New cargo centres and free-zone concepts along the route are early indicators to watch.

Selective repositioning

For producers in São Paulo or Curitiba, Santos remains cheaper in many cases.

But companies with strong Asia-bound exports and flexible location choices may evaluate Mato Grosso do Sul or Paraguay differently from 2028 onward.

Potential Location Shifts

Location logic shifts gradually, not disruptively. Three movements are foreseeable.

From Atlantic-adjacent to Pacific-adjacent options

Mato Grosso do Sul becomes more attractive for processors currently based in Paraná or São Paulo if the logistics disadvantage disappears.

New clusters in peripheral regions

Salta, Jujuy and the Paraguayan Chaco may gain relevance for mining, logistics and corridor-adjacent services.

Asia-focused repositioning

Companies with dominant Asia-bound exports may evaluate locations closer to Pacific routes.

No mass relocation

The effect is selective. For many industrial producers, Atlantic infrastructure and existing supplier ecosystems remain stronger.

Three development paths for the corridor

Scenario A: The corridor remains marginal

Low-impact path · 2026–2028In this scenario, the corridor remains a political symbol without operational impact. Paraguayan and Brazilian exports continue routing through Santos and Paranaguá. The estimated cost savings do not materialise because border crossings remain slow and customs documents are not digitalised.

Implication for EU companies: Do not base any location decision on the corridor. Existing structures in São Paulo and Santos remain optimal.

Scenario B: Regional logistics clusters emerge

Base-case path · 2027–2030The corridor becomes operational but grows more slowly than expected. Mato Grosso do Sul and the Paraguayan Chaco develop into new logistics hubs, mainly for agro and mining. Industrial production remains concentrated in São Paulo.

Implication for EU companies: Selective location review. For agro-tech, mining suppliers and logistics providers, the corridor becomes investment-relevant from 2028. For industry with EU or Atlantic focus, São Paulo and Curitiba remain more relevant.

Scenario C: Stronger Pacific reorientation

High-impact path · 2028–2032In this scenario, the corridor catalyses a broader geopolitical shift. Mercosur becomes more strongly oriented toward Asia as a raw-material and agricultural hub, while new industrial parks emerge in Mato Grosso do Sul, Paraguay and northern Argentina.

Implication for EU companies: Strategic repositioning may be required. Companies active in Mercosur after 2030 should build corridor optionality and avoid relying on one export direction only.

Signals that would make the corridor commercially relevant

Investment signals

Paraguay has invested heavily in the corridor, and Chile has approved long-term infrastructure spending for roads, ports and security. Brazil ratified the TIR Convention in December 2025, effective from July 2026.

Private-sector follow-on investment remains limited. COFCO International is investing in Santos, not Antofagasta — a signal that Chinese players are still betting on Atlantic routes.

Signal: public infrastructure is moving; private capital is still cautious.Trade data

Paraguay's exports to Chile increased in 2024, but most flows still rely on existing Atlantic or Argentine routes. Mato Grosso do Sul exports to Asia remain largely routed via Santos.

TIR reduces administrative friction, but it does not by itself generate freight volume.

Signal: trade flows are shifting minimally, not structurally.Search and engagement patterns

Search interest and LinkedIn engagement around the corridor are rising, especially in Chile, Paraguay and northern Argentina.

International investors, especially from Europe, remain cautious. Real estate interest is rising in corridor regions, but institutional buyers are still missing.

Signal: awareness is rising, but commitment remains limited.Funding programmes

Fonplata and the Inter-American Development Bank support corridor-related infrastructure and planning.

The missing piece is substantial private-sector co-financing: no major PPP wave, no corridor-focused private equity thesis and no large Chinese infrastructure commitment to the road corridor itself.

Signal: public sector builds, private sector watches.Decision framework for EU and international companies

Use the Corredor Bioceánico as a scenario variable, not as a fixed assumption.

For 2026/27, the corridor should not be the primary reason to select or relocate a site. For decisions reaching into 2028–2032, it belongs in the model as potential logistics optionality — particularly for corridor-adjacent operations and Asia-oriented export flows.

The business case still depends on completed infrastructure, reliable border operations, actual freight volume, port capacity and private follow-on investment.

- For new investments in agro, mining and logistics: review corridor-adjacent locations such as Mato Grosso do Sul, the Paraguayan Chaco and Salta/Jujuy. Timing: not before 2027, more realistically 2028/29.

- For existing locations in São Paulo or Curitiba: do not assume relocation is necessary. Compare the corridor with established Atlantic infrastructure, supplier ecosystems and customer access.

- For strategic planning: build the corridor as a hedge. Locations with flexible export routing preserve optionality if the Pacific axis becomes more relevant.

- What not to do: invest only on the basis of government communication. The promised transformation is possible, but not certain.

Bottom line: The Corredor Bioceánico is not a secured operating advantage for 2026/27. It is a relevant structural variable for 2028–2032 and should be included in long-term location models as optionality rather than certainty.

Frequently Asked Questions on the Corredor Bioceánico

Should an EU company include the Corredor Bioceánico in its location analysis in 2026?

Yes, but as a secondary scenario factor rather than a fixed operating assumption. The corridor should be modeled as optionality from 2028 onward and tested against established Atlantic routes, infrastructure gaps, border procedures and actual freight demand.

When will the Corredor Bioceánico be operationally usable for regular freight transit?

This analysis treats regular commercial heavy-freight use before 2028 as unlikely. The decisive conditions are completion of missing road sections, reliable border procedures, customs integration, port capacity and sustained freight volume.

Which sectors and industries benefit most from the Corredor Bioceánico?

Primarily agribusiness, mining, logistics and transport, and selected industrial producers with strong Asia-bound exports. For companies with EU- or Atlantic-focused exports, São Paulo and Santos remain more relevant.

What are the critical early indicators that the corridor is actually working?

Private follow-on investment, measurable trade-volume shifts and institutional logistics or real-estate investment in corridor regions. Without these, the corridor remains primarily a public infrastructure project.

Marcus A. Volz is a Market & Search Intelligence advisor and Latin America SEO consultant for B2B companies. He has lived and worked in Argentina since 2006 and advises companies on Mercosur market entry, international SEO, B2B visibility, AI search visibility and market reality validation.

Evaluating a Mercosur location or logistics decision?

I help companies compare locations, routes, market access, infrastructure risk and commercial visibility before budgets and operating structures are committed.

Request a location assessment