Does the Corredor Bioceánico Reshape Location Logic in Mercosur?

Market Intelligence: Between Infrastructure Reality and Location Decision

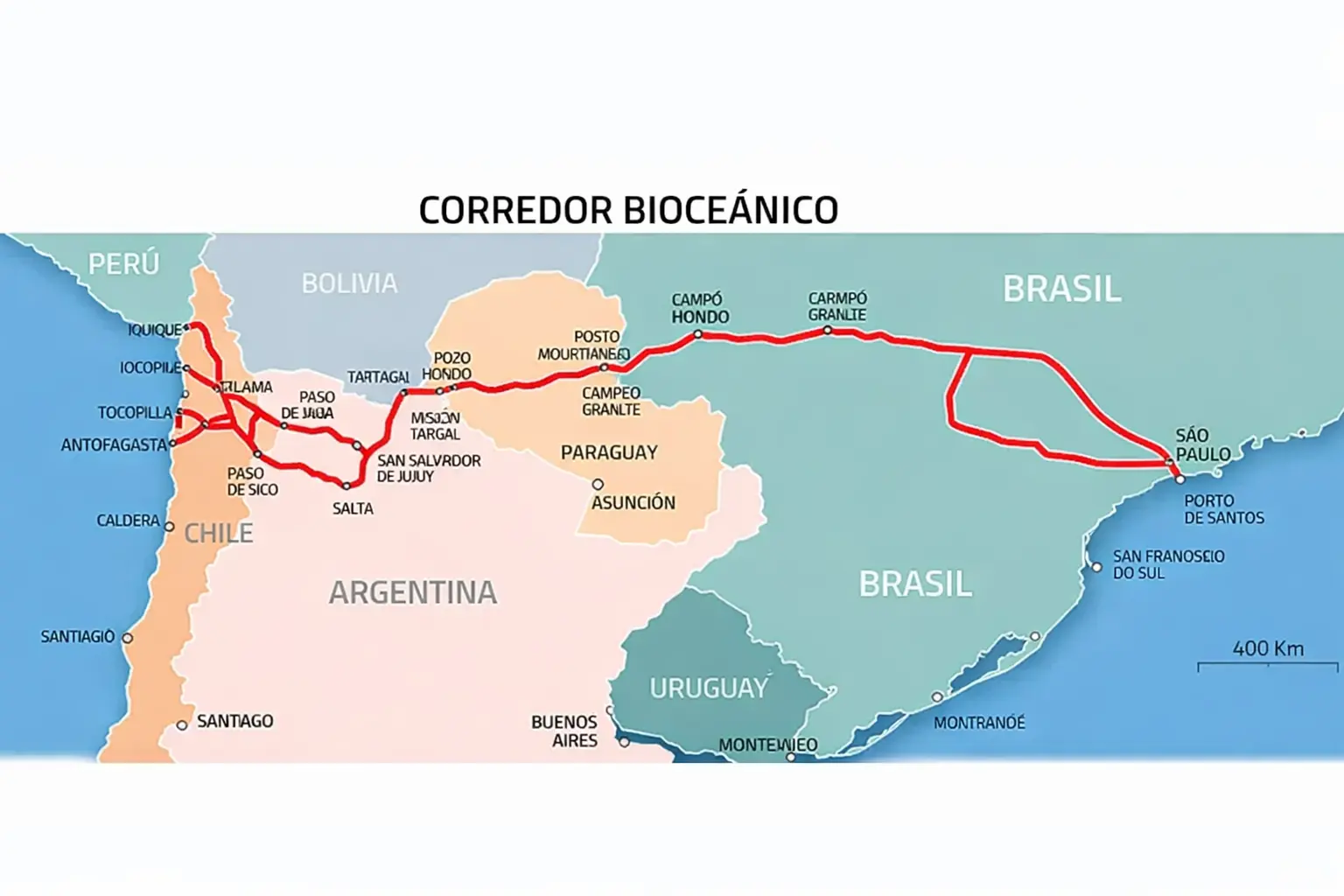

The Corredor Bioceánico Vial is a 2,400 km road connection linking Mato Grosso do Sul (Brazil) through Paraguay and northern Argentina to Chile's Pacific ports of Antofagasta, Mejillones and Iquique. It is projected to cut the export route to Asia by up to 10 days and reduce logistics costs by approximately 20%. The corridor becomes economically relevant for agroindustrial producers, mining suppliers and logistics providers operating in Mercosur with Asia-bound exports. For EU investors with production sites in Brazil or Paraguay, location logic could shift from 2027/28 onward – provided Argentina completes the missing 134 km of Ruta Nacional 51. The current assessment: infrastructure is being built, but critical mass has not yet been reached. The corridor will function, but more slowly than politically communicated and with lower initial impact than projected. The real question is not whether, but when the threshold will be reached at which private follow-on investment begins – and which companies are prepared to invest during the build-up phase.

Structural Analysis

Geographic Axis: Brazil–Paraguay–Chile

The Corredor Bioceánico connects four countries at different stages of completion. Brazil is 90% operational, Paraguay is closing its section by end of 2026 (Puente Bioceánico currently at 82%). Chile is infrastructure-ready and has committed USD 639 million for port modernisation. The critical bottleneck: Argentina. Ruta Nacional 51 between San Antonio de los Cobres and Paso de Sico still lacks 134 km of full asphalt. The route is currently passable with construction machinery and limited freight, but not suitable for regular volume logistics. Salta has applied for Fonplata financing with construction start in 2026, full completion at the earliest in 2028.

As long as this gap remains, the corridor stays a regional project, not a continental game-changer. Investors should not expect operational readiness for regular freight transit before 2028.

Geographic Bottleneck: The corridor is only as strong as its weakest link. As long as Argentina's 134 km remain unpaved, it remains a promise. Investors must not expect operational readiness before 2028.

Export Logic: Atlantic vs. Pacific

Currently, Mato Grosso do Sul exports via Santos and Paranaguá (Atlantic) to Asia via Cape Town or the Panama Canal. Transit time to Shanghai: approximately 54 days. With the Corredor Bioceánico via Antofagasta, the route shortens to 44 days – a time gain of 10 days and a distance advantage of 8,000 km. Logistics costs are estimated to fall by 20%, primarily through shorter sea freight times and avoided canal fees.

Paraguay exported soybeans worth USD 2.5 billion in 2024, routing 37% through Argentina for processing, 18% to the EU, and the remainder to Asia via Argentine ports. With the corridor, Paraguay gains direct Pacific access without Argentine intermediary ports or Brazilian Atlantic routes. For a landlocked country, this is transformative.

For Chile, the corridor means northern ports Antofagasta and Iquique become hubs for Brazilian and Paraguayan agricultural exports. Freight volume could rise to handle 40% of South American meat and grain production – provided the ports have capacity. Antofagasta is currently expanding its Molo de Abrigo, Iquique has installed a new container crane.

Affected Sectors

Agribusiness: Soybeans, corn, beef from Mato Grosso do Sul and Paraguay. Main beneficiaries are processors near the corridor and exporters with Asia focus. Cargill, ADM, COFCO and Louis Dreyfus already control two-thirds of Paraguay's soybean exports – they will reposition their logistics hubs accordingly.

Mining: Lithium, copper, iron ore. Northern Argentina (Salta, Jujuy) and the Paraguayan Chaco hold exploitable deposits. Projects like Taca Taca (copper) and Río Tinto (lithium) in Salta were previously unviable due to logistics costs. Whether the corridor alone lowers the profitability threshold depends on commodity prices, water availability and local permits – not just road access. Infrastructure is necessary but not sufficient.

Logistics & Transport: Freight forwarders, customs brokers, port operators. New cargo centres are emerging along the corridor – Paraguay is planning a Centro Multimodal de Cargas in Güemes, Chile is opening the Zona de Desarrollo Logístico La Negra in Antofagasta with a Paraguayan free zone.

Industry: Auto parts, machinery, chemicals. For producers in São Paulo or Curitiba, Santos remains cheaper. But for companies exporting to Asia with flexible location choices, Mato Grosso do Sul becomes more attractive – lower land costs, shorter logistics chains, proximity to raw materials.

Potential Location Shifts

Location logic shifts gradually, not disruptively. Three movements are foreseeable.

First: From Atlantic-adjacent to Pacific-adjacent production sites. Mato Grosso do Sul becomes more attractive for processors currently based in Paraná or São Paulo. Land costs in Campo Grande are 40% below São Paulo, labour costs 25% lower. If the corridor functions, the logistics disadvantage disappears.

Second: New cluster formation in previously peripheral regions. Northern Argentina (Salta, Jujuy) and the Paraguayan Chaco were economically marginal. Argentina under Milei has achieved macroeconomic stability since 2024 – inflation fell from 211% to 32%, the fiscal budget is balanced, and the RIGI investment regime for major projects is active. This makes Salta/Jujuy calculable for mining investments for the first time. Paraguay benefits simultaneously: real estate investors are buying land in the Chaco – expectation: value appreciation of 200–300% in five years once the corridor is operational.

Third: Industrial repositioning with Asia focus. Companies with dominant Asia-bound exports (over 70% of volume) are evaluating locations closer to the Pacific. This particularly affects agrotech processors and mining suppliers. The effect is selective – mass relocations will not occur, but strategic repositioning begins from 2028.

Scenarios: Three Development Paths

Scenario A: Negligible Effect (20% probability, time horizon 2026–2028)

In this scenario, the corridor remains a political symbol without operational impact. Paraguayan and Brazilian exports continue routing through Santos/Paranaguá. The estimated 20% cost savings do not materialise because border crossings remain slow and customs documents are not digitalised. Investors hold back, no new locations emerge. The Chaco remains peripheral.

Implication for EU companies: Do not base any location decision on the corridor. Existing structures in São Paulo/Santos remain optimal. Break-even for new investments in Mato Grosso do Sul or Paraguay deteriorates.

Scenario B: Regional Cluster Formation (55% probability, time horizon 2027–2030)

The corridor becomes operational but grows more slowly than expected. Freight volume increases annually by 15–20%, not 40%. Mato Grosso do Sul and the Paraguayan Chaco develop into new logistics hubs – but only for agro and mining. Industrial production stays in São Paulo. Location shifts happen selectively: processors with Asia focus and long supply chains migrate westward, but the majority of industry remains Atlantic-oriented.

New clusters emerge along the corridor: Campo Grande becomes an agro-tech hub, Loma Plata (Paraguay) a logistics centre, Salta/Jujuy (Argentina) a mining services location. These clusters are real but small – they complement existing structures without replacing them.

Implication for EU companies: Selective location review. For agro-tech, mining suppliers and logistics providers, the corridor becomes investment-relevant from 2028. For industry with EU or Atlantic focus, São Paulo/Curitiba remains optimal. Timing: do not be first mover, but evaluate from 2028.

Scenario C: Strategic Reorientation Toward Asia (25% probability, time horizon 2028–2032)

In this scenario, the corridor catalyses a broader geopolitical shift. China finances the Corredor Ferroviario Bioceánico (Santos–Chancay/Peru) as a complement to the road corridor, invests in port infrastructure and builds commodity processing capacity inland. Mercosur becomes a raw material and agricultural hub for Asia, while EU exports stagnate.

Location decisions shift fundamentally: production sites move from the Atlantic to the Pacific axis. New industrial parks emerge in Mato Grosso do Sul, Paraguay and northern Argentina. The entire value chain – from raw material extraction through processing to export – reorients westward. Capital allocation follows: private equity and infrastructure funds invest heavily in corridor-adjacent assets.

Implication for EU companies: Strategic repositioning required. Companies wanting to remain active in Mercosur after 2030 must build corridor optionality. This means: locations with flexible export routing (both Atlantic and Pacific), partnerships with Chinese logistics providers, securing early-mover advantage in emerging clusters. Risk: missed transformation if competitors move faster.

Early Indicators: What Market Intelligence Shows

Investment Signals

The data shows selective but real investments. Paraguay has invested USD 1.1 billion in the corridor, including USD 443 million for Tramo 1, USD 354 million for Tramo 3, USD 90 million for the Puente Bioceánico. Chile has approved USD 639 million over 10 years for roads, ports and security. Brazil ratified the TIR Convention in December 2025 – effective from July 2026, enabling simplified customs clearance.

Private sector investments: COFCO International (China) is investing USD 486 million in port expansion in Santos, not in Antofagasta – a signal that Chinese players are still betting on the Atlantic route. Real estate developers are buying land in the Chaco, but volumes remain below USD 100 million – speculation, not production relocation.

Signal: Public infrastructure is being built, private follow-on investment is still absent. This points to Scenario B: gradual development, no disruption.

Trade Data

Paraguay's exports to Chile rose 35% in 2024 to approximately USD 700 million, primarily beef. The majority still routes through Argentine Atlantic ports, not through the corridor. Brazil's exports from Mato Grosso do Sul to Asia remain 90% via Santos. In the border town of Assis Brasil (Acre), exports rose 130% in Q1/2025 – but this is a statistical outlier, not a structural trend.

Brazil's TIR ratification (December 2025, effective July 2026) enables simplified customs clearance for international freight transit – a technical prerequisite for functioning corridor operations. But TIR alone does not generate freight volume; it only reduces administrative friction.

Signal: Trade flows are shifting minimally, not fundamentally. The promise of "40% of South American agricultural production via Pacific" is not visible in data as of February 2026. Growth is occurring but at niche level.

Search and Engagement Patterns (Proxy for Business Interest)

Search queries for "Corredor Bioceánico inversiones" rose 80% in 2024/25 – dominated by regional media, not international investors. LinkedIn engagement on corridor content comes primarily from Chile, Paraguay and northern Argentina – but barely from São Paulo or Europe. This means: regional actors are active, international investors remain cautious.

Real estate portals show rising interest in land near Carmelo Peralta, Loma Plata and Pozo Hondo – but no institutional buyers, only individual investors. That is speculation, not industrial location development.

Signal: Awareness is rising, commitment is absent. Companies are watching but not investing. Timing question: who jumps first?

Funding Programmes

Fonplata (development bank of ARG, BOL, BRA, PRY, URY) finances Paraguayan and Argentine corridor sections with a total of USD 450 million. The IDB (Inter-American Development Bank) coordinates the Plan Maestro Regional de Integración. These multilateral institutions are not risk-takers – their involvement signals: the project is technically feasible, politically desired, but financially fragile.

What is missing: substantial private sector co-financing. No PPPs (Public-Private Partnerships) announced, no private equity funds with corridor focus, no Chinese infrastructure investments in the road connection itself (COFCO invests USD 486 million in Santos port, not Antofagasta). Private capital is waiting. This absence is the most critical signal: institutional investors see no bankable business model yet.

Signal: Public sector builds, private sector watches. This is typical for infrastructure Phase 1. But without follow-on investment, the corridor remains a political project, not an economic multiplier.

Conclusion: The Decision Question for EU Companies

Should an EU company include the Corredor Bioceánico in its location analysis – yes or no?

Answer: Yes, but not as a primary factor – rather as optionality from 2028.

Infrastructure is emerging, but more slowly and at smaller scale than communicated. Companies investing in Mercosur today should model corridor scenarios but not base decisions on them. Concretely this means:

For new investments in agro, mining, logistics: Review corridor-adjacent locations (Mato Grosso do Sul, Paraguayan Chaco, Salta/Jujuy). Timing: not before 2027, optimal 2028/29 – when Ruta 51 is complete and first freight volumes are flowing.

For existing locations in São Paulo/Curitiba: No relocation needed. The corridor does not replace Atlantic routes, it complements them. Only when Asia-bound exports dominate (over 70% of volume) does Pacific proximity become relevant.

For strategic planning: Build the corridor as a hedge. Choose production locations with flexible export routing (e.g. Mato Grosso do Sul with access to both Santos and Antofagasta). This maintains adaptability if Scenario C materialises.

What EU companies should not do: invest on the basis of government communications. The promised "transformation" is possible, but not certain. Those who invest in the Chaco in 2026 because Chile and Paraguay promise it bear the Argentina risk and port capacity uncertainty alone.

Bottom Line: The Corredor Bioceánico is not a game-changer for 2026/27, but a structural factor for 2028–2032. Companies defining location logic for the next decade must include it – not as certainty, but as optionality. Those who ignore the optionality lose strategic flexibility. Those who invest too early pay pioneer premiums without secured returns.

Frequently Asked Questions on the Corredor Bioceánico

Should an EU company include the Corredor Bioceánico in its location analysis in 2026?

Yes, but not as a primary factor – rather as optionality from 2028 onward. Infrastructure is being built, but critical mass for commercial volume logistics is still missing. Companies should model corridor scenarios but not base decisions on them. For new investments in agro, mining or logistics: evaluate corridor-adjacent locations from 2027/28. For existing locations in São Paulo/Curitiba: no relocation needed as long as Asia-bound exports remain below 70% of volume. Strategically: build the corridor as a hedge through flexible export routing.

When will the Corredor Bioceánico be operationally usable for regular freight transit?

For regular commercial heavy-freight traffic, not before 2028. The critical bottleneck is Argentina: Ruta Nacional 51 between San Antonio de los Cobres and Paso de Sico still lacks 134 km of full asphalt. The route is currently passable with construction machinery and limited freight, but not suitable for regular volume logistics. Salta has applied for Fonplata financing with construction start in 2026. In parallel, Brazil's TIR Convention ratification must become effective in July 2026 to enable simplified customs clearance.

Which sectors and industries benefit most from the Corredor Bioceánico?

Primarily four sectors: Agribusiness – soybeans, corn, beef from Mato Grosso do Sul and Paraguay with Asia-bound exports. Mining – lithium, copper in northern Argentina (Salta, Jujuy), provided commodity prices and water availability allow. Logistics & Transport – freight forwarders, customs brokers, new cargo hubs. Industrial producers with over 70% Asia-bound exports evaluating flexible locations. For companies with EU- or Atlantic-focused exports, São Paulo/Santos remains optimal.

What are the critical early indicators that the corridor is actually working?

Three measurable indicators: First, private follow-on investment – PPPs, private equity funds or Chinese infrastructure investments in corridor-adjacent assets. Status as of February 2026: completely absent. Second, trade volume shift – when Mato Grosso do Sul exports measurably reroute from Santos to Antofagasta (currently 90% still via Santos). Third, real estate and logistics investments in corridor regions by institutional investors, not just speculators. As long as these three are missing, the corridor remains a political project without economic multiplier effect.

Market Intelligence for Mercosur Location Decisions

This analysis is part of my ongoing Market Intelligence monitoring for companies with Mercosur expansion plans. The Corredor Bioceánico is a test case for a central question: when does infrastructure promise become investment reality?

I work with companies that need to distinguish between hype and substance – and that require strategic optionality when markets move faster than expected.

Typical questions:

- When is a corridor operational – not politically announced, but factually usable?

- Which early indicators show whether private investors are following or holding back?

- How do you build location optionality without committing too early?

- Which scenarios justify which timing decisions?

These are not questions for desktop research. They require continuous monitoring of investment announcements, trade data, construction progress and political shifts.

If you are preparing Mercosur location decisions for 2026–2030:

→ Market Intelligence & Location Strategy

Planning investments in Brazil, Paraguay or Argentina?

Let's talk about strategic location analysis – before budget is committed.

Contact: info@volzmarketing.com