Mining, Lithium & Critical Minerals in Mercosur

Market & Search Intelligence for mining suppliers, lithium technology providers, process technology firms, environmental engineering companies and industrial B2B suppliers evaluating Mercosur and adjacent South American mining corridors.

Updated in June 2026: mining exports, lithium and copper projections, RIGI timing, lithium ramp-up, critical minerals and AI-assisted supplier visibility.

What matters in practice

- Which mining cluster, operator and project stage fit the supplier offer?

- Is the realistic buyer an operator, EPC, subcontractor or local partner?

- Which technical proof reduces procurement risk before first contact?

- How visible is the offer in Spanish, Portuguese and AI-assisted supplier research?

- Which next step is useful before travel, budget or partner outreach?

in 2025

over ten years

production in 2025

under Decreto 105/2026

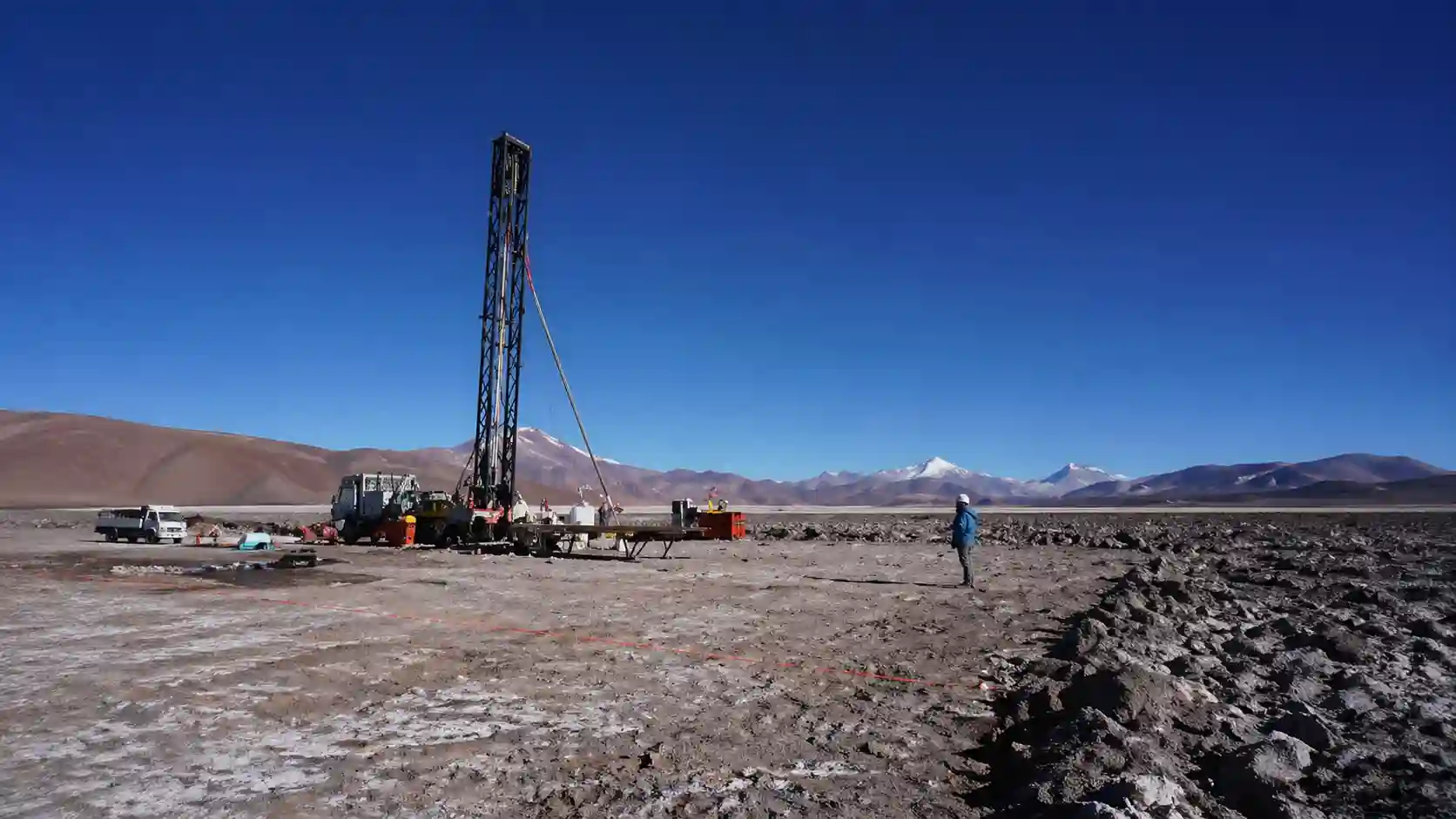

Mining and critical minerals in Mercosur: where suppliers fit into the project chain

For mining, lithium and critical-mineral suppliers, Mercosur is not only an investment story.

The practical question is whether operators, EPCs, subcontractors, procurement teams, local partners, search engines and AI systems can understand where the supplier fits, which operating problem it solves and why it should be considered.

Lithium, copper, gold, rare earths, critical minerals, water treatment, process technology, automation, sensors, environmental engineering and mining services create different demand layers. A supplier becomes relevant when its offer is connected to a concrete cluster, project stage, operating constraint and procurement path.

How VolzMarketing reads the mining sector

No EPC work, no engineering design and no procurement brokerage — but a strategic reading of market logic, supplier visibility and the next useful decision.

Cluster and market-fit reading

Assessment of how the supplier fits into lithium, copper, gold, rare-earth or industrial mining contexts: cluster, project stage, operator environment and technical application.

Operator, EPC and procurement mapping

Reading of operators, EPCs, subcontractors, engineering firms, local partners and procurement structures that need to understand the offer.

Search and AI visibility diagnosis

Review of search results, visible competitors, public sources, local-language supplier research and AI-generated answers related to the company, sector and market.

Trust signals and technical proof

Recommendations on documentation, references, certifications, operating-context proof, local signals, partner proof and content elements that reduce buyer uncertainty.

What the current mining context changes

Mining and lithium are becoming more concrete as investment, project timing and export expectations move from general potential to supplier-relevant execution questions.

Argentina is no longer only a lithium headline

Export records, copper expectations, lithium ramp-up and RIGI timing make Argentina relevant for suppliers across process technology, water, energy, engineering, logistics and technical services.

Procurement follows clusters, not countries

Lithium in the Argentine northwest, copper in San Juan, gold in Patagonia and rare-earth or industrial-mineral logic in Brazil create different buyer paths and proof requirements.

Supplier visibility becomes part of market access

Operators, EPCs and subcontractors increasingly research suppliers through local-language sources, technical queries and AI-assisted discovery before formal contact begins.

What a mining buyer checks before considering a supplier

In mining markets, a technically strong offer is not enough. Buyers must quickly understand technical fit, project relevance, local feasibility and operational proof.

Cluster and project stage

Does the supplier fit lithium brine, copper development, gold operations, rare-earth processing, iron ore, industrial minerals or adjacent infrastructure?

Buyer and procurement path

Is the realistic path operator access, EPCs, subcontractors, engineering firms, local industrial partners or service providers?

Operating conditions

Altitude, brine chemistry, water stress, dust, energy access, remote logistics, corrosion and maintenance capacity can change supplier relevance.

Documentation and proof

Which technical documents, certifications, case references, safety information, environmental proof and local service capacity are visible?

Local market fit

Which country, province, mining corridor, regulatory setting, project stage and partner structure are relevant for the offer?

Search and AI visibility

Does the supplier appear when buyers research mining equipment, lithium technology, process solutions or local supplier options in Spanish, Portuguese and English?

Mining and sector sources, updated in June 2026

These sources provide the public market context. The service assessment does not repeat a generic country overview; it translates the context into buyer, supplier, visibility and decision logic for a specific company.

- Panorama Minero: Argentina mining exports and 2026 mining-sector context.

- Argentina.gob.ar: Decreto 105/2026 extending the RIGI application period.

- Eramet Integrated Report 2025/2026: Centenario lithium production and 2026 ramp-up expectation.

- Reuters: Argentina lithium and copper export projection and mining investment outlook.

- Reuters: Rio Tinto, Nuton and Los Azules copper project context.

- CEBRI: Brazil critical and strategic minerals context, rare earths and Serra Verde.

- U.S. International Trade Administration: Brazil mining sector overview.

Econosur provides South American sector and market context. VolzMarketing translates that context into service logic for companies: which market assumptions hold, which buyer layer matters, which proof is missing and how a supplier appears in search and AI-assisted research.

From mineral potential to visible supplier logic

The value is not to repeat mining potential. The value is to make a concrete supplier role readable across market context, search results, source spaces and AI systems.

Market Reality

Which cluster assumptions are plausible, which project dynamics matter and which local constraints change the company’s priorities?

Buyer & Partner Logic

Which operators, EPCs, subcontractors, partners, distributors or procurement teams need to understand the supplier offer?

Search & AI Visibility

Which terms, sources, entities and proof signals decide whether the company is correctly understood in search and AI-generated answers?

Related VolzMarketing pages

- Explore other Mercosur industry lenses

- Evaluate Mercosur market entry and expansion

- Use market analysis for mining and supplier decisions

- Build a market-entry strategy for mining-related offers

- Understand partner, distributor and buyer network logic

- Connect market intelligence, search and AI visibility

Assess mining, lithium or critical-mineral supplier visibility in Mercosur

Send the company website, target market, sector role, product or service, relevant clusters, intended buyers and current market-entry questions. The assessment reviews market relevance, operators, EPCs, partners, search visibility, AI visibility and next steps.

1. Market

Country, cluster, project stage, operator context or mining corridor.

2. Offer

Technology, equipment, process solution, engineering service or supplier role.

3. Decision

Validation, procurement path, visibility, positioning or investment priority.

No EPC work, no engineering design, no legal advice, no procurement brokerage, no customs handling, no local representation and no operational project management.

VolzMarketing is a specialised consultancy for Market & Search Intelligence, international B2B visibility and digital market analysis. The focus is how companies are understood in search engines, AI systems, source spaces and international markets — not only through rankings, but through market logic, entities, proof and clear strategic interpretation.

volzmarketing.com